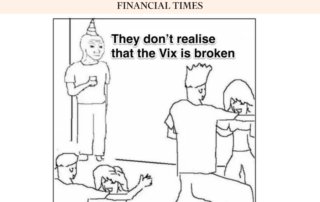

Alphacution Press: FT on “The Broken VIX”

We know things are going pretty well when an Alphacution guest post by derivatives specialist Don Dale is referenced by the Financial Times. See Robin Wigglesworth's "The 'Broken' VIX."

We know things are going pretty well when an Alphacution guest post by derivatives specialist Don Dale is referenced by the Financial Times. See Robin Wigglesworth's "The 'Broken' VIX."

Guest Post: Derivatives specialist, Don Dale, offers a thoughtful case for why the CBOE Volatility Index (VIX) is not broken, despite punditry claims to the contrary. Two pearls of wisdom, up front: 1) Pundits like to complain; and, 2) Be careful what you wish for!

"For every action in nature there is an equal and opposite reaction." - Sir Isaac Newton The performance - or, health - of complex systems is difficult to measure. Typically, you need deviations from norms across numerous sensors - the analytics - converging to signal whether a complex system is functioning properly or not. Add the inevitability of change, and the task becomes exponentially more challenging as continuity of measurement over time decays... And then, there's the stuff that's difficult to measure, if it's measured at all. The intangibles. The slippage factors that don't come into play until they do. Like, a global pandemic - or when a frustrated segment of the population spills out into the streets in cities - big and small - across the landscape... The indicators most commonly used to signal the health of our complex markets may no longer serve their stated purposes. For instance, does the VIX still measure fear? Aside from today's notable spike, the equity markets appeared to have returned to normal volatility [...]

"It is action, not rest, that constitutes our pleasure." - John Adams Amidst the doom and uncertainty of any unfolding saga, there are always bright spots, if you know where to look. After all, every problem can be an opportunity in disguise. And so, besides the uptick in all things online relative to most things not online during a pandemic lockdown, the expectation has been that there would be some bright spots for listed market first responders - the market makers and high-turnover arbitrageurs - given the unprecedented volatility that erupted in global markets in late February. This week, Alphacution has begun to confirm some of those expectations as critical data necessary to fill in the picture of what actually happened below the unprecedented volatility headlines began flowing... To create the proper gravity of perspective, let's start with average daily volume (ADV) in US cash equity markets for March arriving at more than 15.6 billion shares. This is an all-time high and a level not even remotely approximated since the [...]

"The struggle itself towards the heights is enough to fill a man's heart. One must imagine Sisyphus happy." - Albert Camus "Captain Jack will get you high tonight And take you to your special island Captain Jack will get you by tonight Just a little push, and you'll be smilin'." - Billy Joel This one has a long fuse, but you might enjoy the customary overallocation of pictures as we get into it: In a March 22nd note entitled "The Great Leverage Unwind" published by Guggenheim Investments, Global CIO Scott Minerd estimates the impact of the COVID-19 pandemic like this: "...we would need to see about $4.5 trillion of quantitative easing (QE) before everything was resolved. This is in addition to emergency lending through the discount window, dealer repo operations, central bank liquidity swaps, and the Commercial Paper Funding Facility, Primary Dealer Credit Facility, and Money Market Mutual Fund Liquidity Facility. That would take the Fed’s balance sheet to at least $9 trillion, or about 40 percent of last [...]

“It’s not bragging if you can back it up.” – Muhammad Ali While so many seem to be pleasuring themselves with the Tiger King, some of us continue to geek out with the latest data. Now, with March so freshly in the review mirror, certain monthly and quarterly data updates are going to be among our first chances to benchmark the significance of what has just happened in capital markets. We started with a focused comparison of the volatility patterns of the GFC period to the unfolding CVP period here and here, and then detailed the first trading casualties of that volatility here, here and here. Below, is our latest visual of that volatility comparison, where we are beginning to break down the components of volatility represented by the gap and range... Among the more fascinating aspects of this perspective is the illustration that there have been 8 volatility spikes with intraday ranges greater than 20 VIX points since January 2008, and the greatest of these occurred on February [...]

“You can't connect the dots looking forward; you can only connect them looking backwards. So you have to trust that the dots will somehow connect in your future. You have to trust in something – your gut, destiny, life, karma, whatever." - Steve Jobs In an article published today (March 26) by Risk.net based on a statement also released today from ABN AMRO (below), new details about the demise of Ronin Capital emerge - along with that of a "mysterious second default." According to Risk.net, a spokesperson for ABN AMRO has repeatedly suggested Ronin was not the source - a US client - of the $200 million (net) loss. It's just a matter of time now before we learn of another potential victim of this latest volatility spike... ++++++ Update 9:59PM NYC: Well, that was fast! The source of $200 million loss revealed by Risk.net as New York-based Parplus Partners, an equity volatility hedge fund with close ties to Ronin... Until next time, stay safe out there...

“Do what you can, with what you have, where you are.” - Theodore Roosevelt In last week's Feed post, "Marketquake: The Volatility of Volatility," we set up a comparison of volatility levels - and duration - from the GFC with that of the current pandemic period. In that, I implied that elevated volatility persisted for 218 trading days after the initial GFC shock. In other words, it took about 218 trading days for the VIX to traverse the round trip from normal vol levels (~mid-20's) through the associated shocks and back to normal. The chart below is a picture of that path along with where we are as of today, 23 trading days into the latest market shock... Now, 218 trading days into the pandemic shock puts us into early January 2021. The problem, however, is that with the latest vol shock being faster and higher than that of the GFC - and the likelihood that there will be subsequent shocks from the combined ongoing health and economic impacts [...]

“If it be now, tis not to come, if it be not to come, it will be now; if it be not now, yet it will come. The readiness is all." - Shakespeare: Hamlet Act 5, Scene 2 UPDATE HERE (3/26/2020) Last Friday, March 20, CNBC was first to report that "one of the CME’s direct clearing firms was unable to meet its capital requirements. The move forced the exchange to step in and invoke its emergency protocols to auction off the portfolios. Ronin Capital, based in Chicago, was confirmed to be the firm in question, according to sources. Additional sources said Ronin’s problems stemmed from positions in futures tied to the CBOE Volatility Index (VIX)." In concert with Alphacution's recent feed post, "Marketquake: The Volatility of Volatility," on unprecedented volatility levels that surpass that of the 2008-2009 Global Financial Crisis (GFC) period, I wanted to assemble whatever we could on Ronin. A story not well known outside of Chicago prop trading circles, John S. Stafford, Jr. - the founder of [...]

“To develop a complete mind: Study the art of science; study the science of art. Learn how to see. Realize that everything connects to everything else” – Leonardo da Vinci If there was ever a moment in time when we realized just how much everything connects to everything else - a quote (and concept) I have been using to repeatedly bludgeon you lo these many past months - now would be that moment. However, so as not to jump on the singularly overcrowded bandwagon of doom that is the current events flow of content (for now), I'd like to walk through a storyboard of related significance. That sadly familiar aroma in the air is fear; a specific vintage of which has not washed over the market ecosystem since 2008. Many are coming to the conclusion that if the virus doesn't take us down, the arsenal of preventative measures just might - and therefore, one way or another, we are likely entering a period of financial stress (to put it as [...]