Feed

Reports

About

Company

Founder

Contact

Login / Subscribe

Markets. Trading. Technology.

On the Feed

For Subscribers

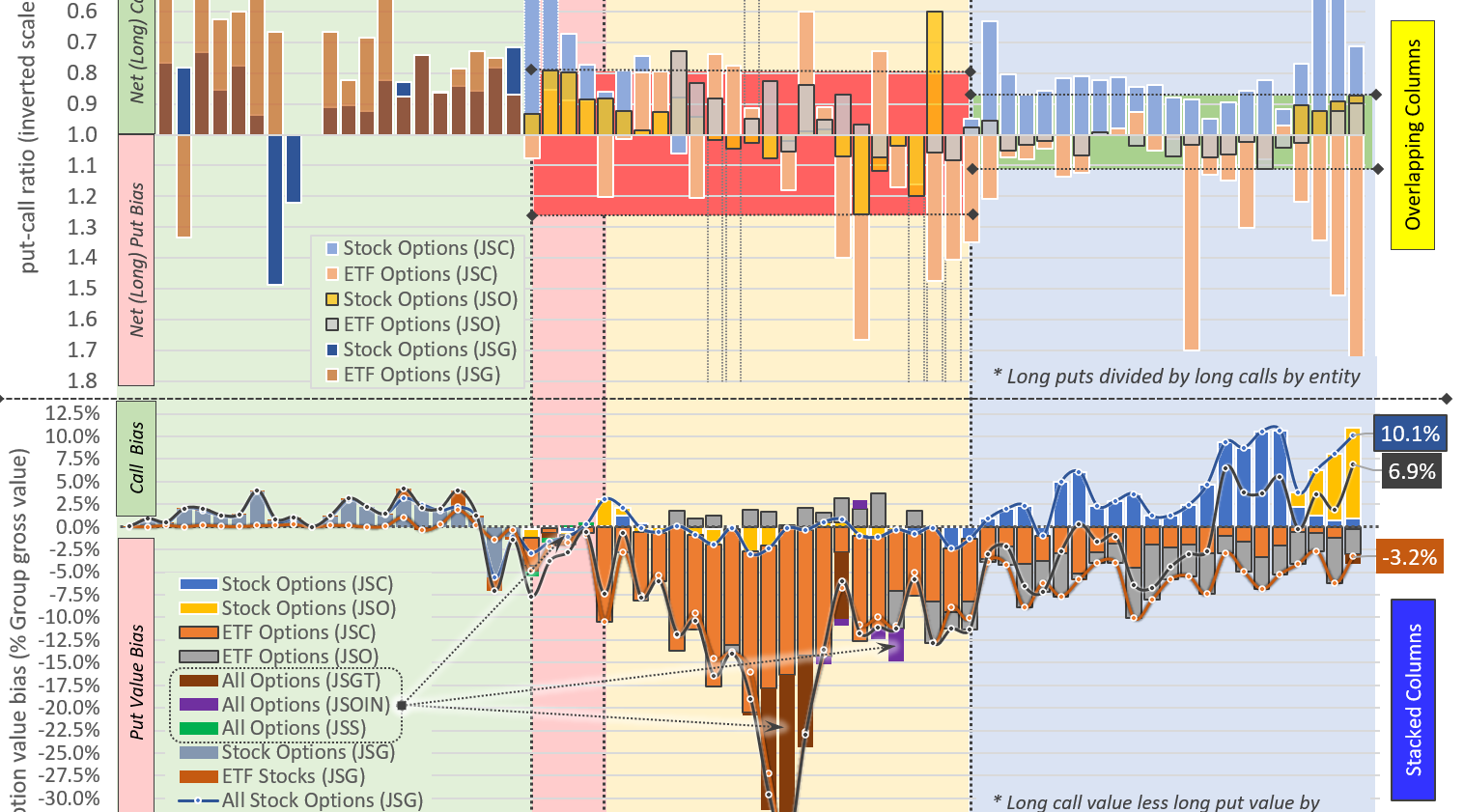

Measuring Structural Alpha Capacity in the Global ETP Market

March 30, 2021

Open

Case Study: History of Jane Street

May 28, 2020

For Subscribers

Blast Off: First Look at Q1 First Responders

April 23, 2020

For Subscribers

Virtu Financial: Musical Chairs

February 13, 2020

For Subscribers

A Brawl Breaks Out in the Futures Market – Part 2

October 11, 2019

For Subscribers

Tradebot Systems: There’s Still Room Under the Radar

October 3, 2019

For Subscribers

Virtu Financial: The Frying Pan and the Fire

August 22, 2019

For Subscribers

When #ETFs Ate The Beta

November 11, 2018

Open

Those Fees Are No Laughing Matter!

September 16, 2018

For Subscribers

Exposing Franklin Templeton’s Greatest Challenge: #ETFs

August 14, 2018

Posts pagination

« Previous

1

2

Company

Find out more about what we do

GO

Founder

Where the Alphacution vision starts

GO

Contact

Reach out to us anytime

GO

Receive updates on Alphacution's latest research.

Get Newsletter