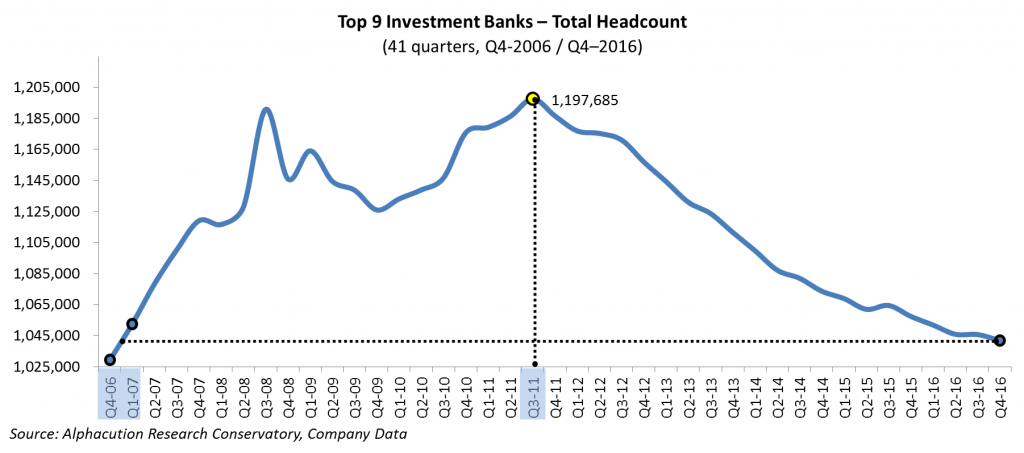

Well, it would have been the Top 10 investment banks, but @Barclays doesn’t publish quarterly headcount for some reason. Maybe they will help us fix that.

Anyway, for the Top 9 investment banks, total headcount is down 13% from its peak in Q3 2011. And, with at least 2 of the 9 – @Deutsche Bank and @CreditSuisse – reporting significant headcount reductions for the road ahead as part their year-end 2016 financial releases and 2017 guidance, it’s not much of a stretch for us to predict that the Wonkavator is highly likely to travel further back in time than year-end 2006 (see below).

I just want to let this picture dangle for a bit without much comment. We will be revisiting and significantly expanding this analysis in the weeks and months ahead as we roll into the development of our 2nd Annual Global Bank Technology Spending study. Stay tuned…