“The voyage of discovery is not in seeking new landscapes, but in having new eyes.” – Marcel Proust

I had hoped to be able to publish the executive summary to our latest case study on Two Sigma this week, however instead, here is one of the more fascinating findings from that research (that we explore in detail in that case study) in the form of a puzzle:

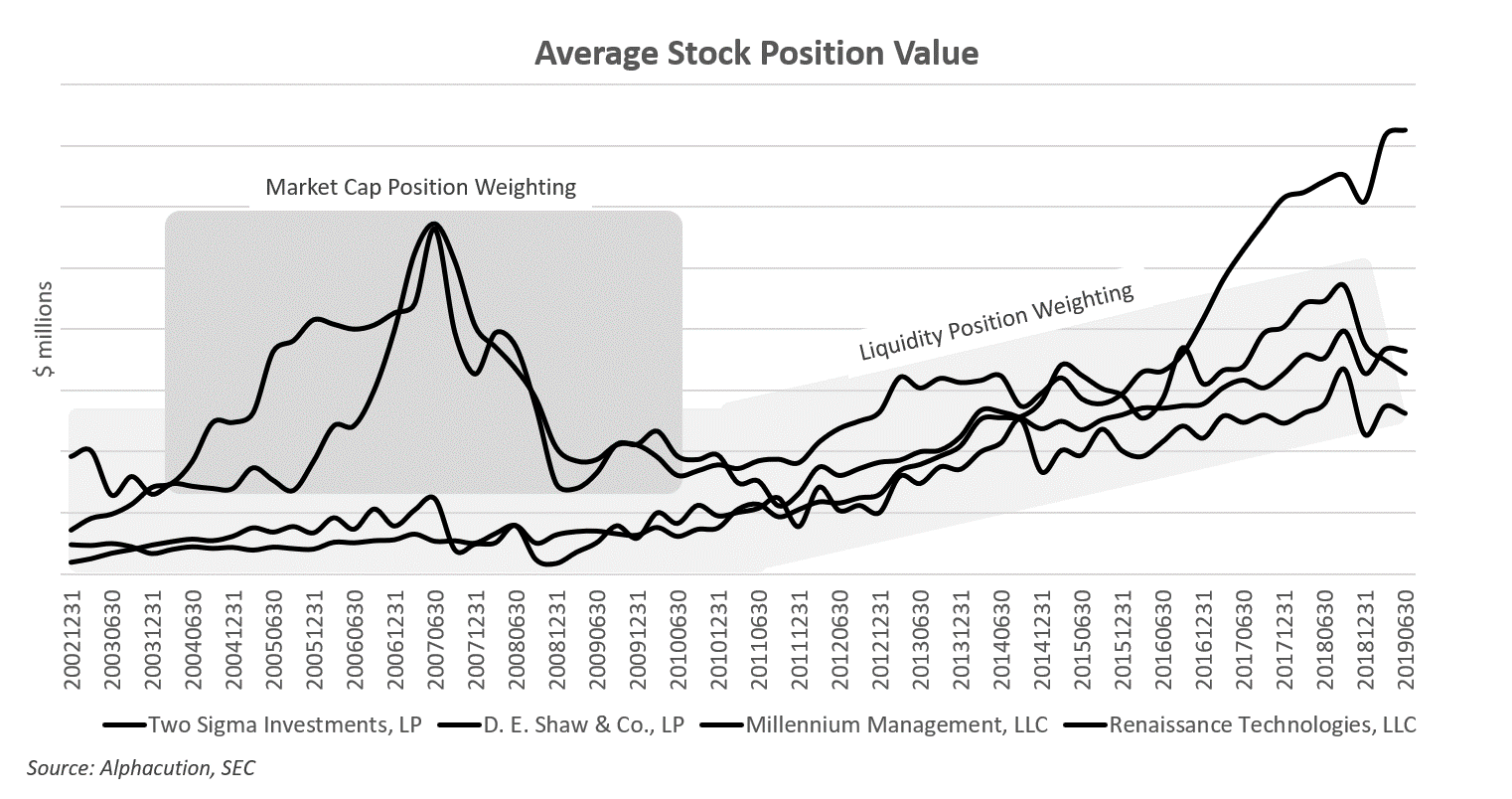

In the chart below, Alphacution presents the average stock position by value for the 67-quarter period beginning Q4 2002 and ending Q2 2019 for the four legendary quant managers, Renaissance Technologies, Millennium Management, D. E. Shaw & Co., and Two Sigma Investments.

What’s fascinating here is how these four leaders, with their core strategies in equities, assembled their portfolios. Four managers with two methods for implementing position sizing; one method based on market capitalization weighting, the other based on liquidity weighting…

Which manager is associated with which method?

One more thing: If you think this is too deep in the weeds for where you are sitting right now, read this.