“…We are not now that strength which in old days

Moved earth and heaven, that which we are, we are;

One equal temper of heroic hearts,

Made weak by time and fate, but strong in will

To strive, to seek, to find, and not to yield.”

– from “Ulysses” by Alfred, Lord Tennyson

“It ain’t about how hard you hit, it’s about how hard you can get hit and keep moving forward. How much you can take and keep moving forward. That’s how winning is done!”

– Rocky Balboa

The clues can be very subtle, but they are there – if you choose to pay close enough attention. We stumbled over one such clue recently. Or, did that clue somehow announce itself to us? You be the judge…

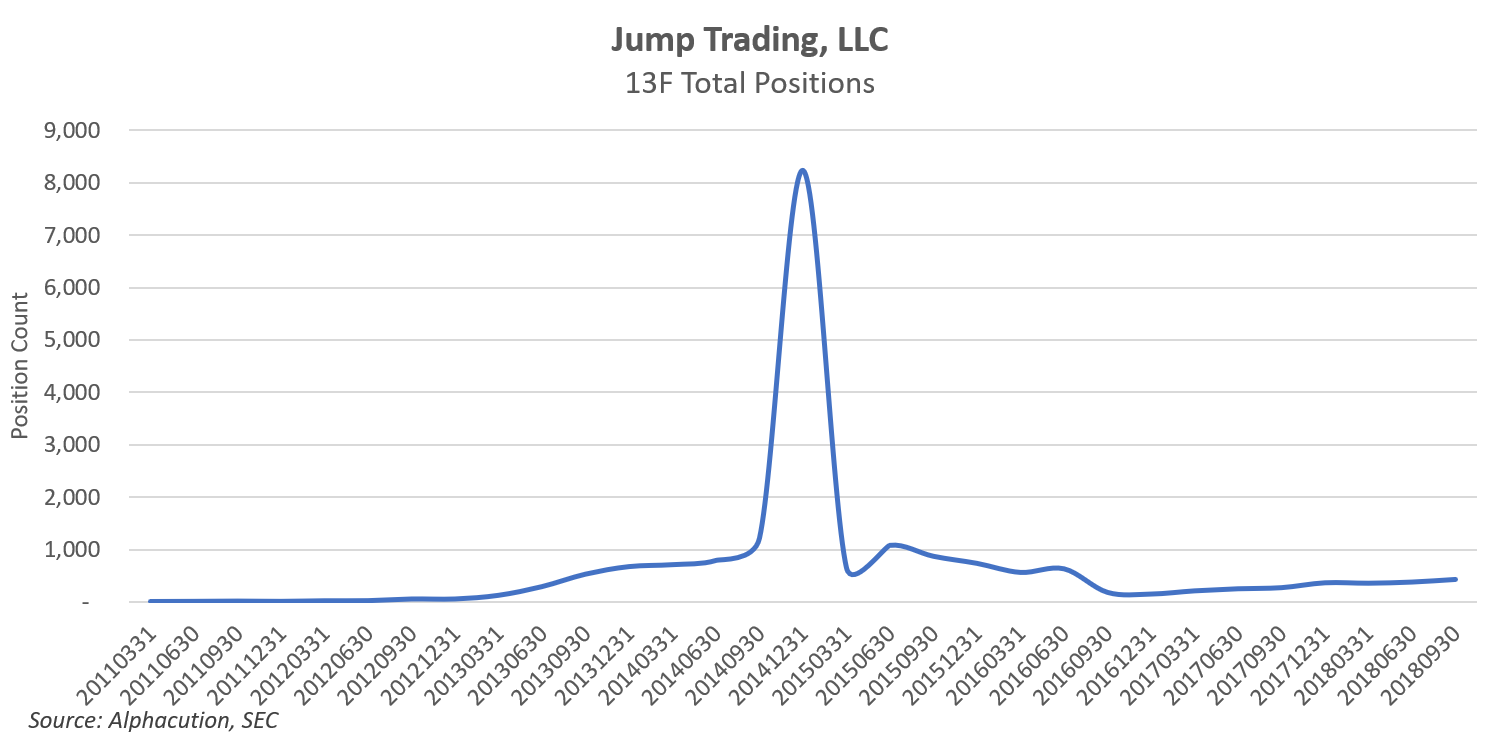

Here’s the setup: In January 2019, Alphacution published a post entitled, “Jump (Experiments In) Trading, LLC” wherein we note, among other highlights, that there may have been a mistake in one of their 13F filings; specifically, a report for Q4 2014. In the exhibit below, Alphacution presents a 31-quarter sample of total 13F positions for Jump Trading – the Chicago-based proprietary powerhouse known more for its high-speed futures trading strategies than those in the 13F securities universe – beginning Q1 2011 and ending Q3 2018. The position spike in Q4 2014 – from a status quo of about 1,000 (13F long) positions to over 8,000 positions – represented a technical error due to disaggregated reporting of option positions. See below…

With the previous quarterly 13F report (for Q3 2014) showcasing total positions of 1,225 (875 of which were due to long call and put option positions), the subsequent Q4 2014 report shows total positions skyrocketing to 8,245 (8,003 of which were attributable to long call and put option positions) before falling back to a level of 659 positions for Q1 2015.

Now, the raw data may be accurate behind all these disclosures – we have no reason to believe otherwise – however, 13F reporting rules only require aggregated disclosure of (long) option positions. In other words, if there is a mistake here, its one of excess transparency. Ok, now, bookmark that thought for a minute…

This is where our story needs to take a radical – and, intensely personally – detour with the following setup (but, rest assured that we will return, full circle, to where we left off): The night of July 7, 2017 started like most other Friday nights for me, but certainly didn’t end there. Halfway into a late night dog walk, the initial drumbeat of rain arrived with an increasing tempo. Prince, the Rhodesian Ridgeback – notoriously averse to getting wet – dragged me and our cadence to somewhere between a speed-walk and an outright run for the remaining few blocks. As I stepped off the curb to cross the street into the final leg home, the lights went out. My next memory is of sitting, scraped and bloodied, in the big stuffed chair in my bedroom…

The cause of this lapse? A congenitally-faulty aortic heart valve; a birthright passed down from my dad (and likely his dad, too) that I never knew I had after 51 consecutive years of active living. It turns out, however – with my brain shutting down due to lack of oxygenated blood flow and as if my eyes had simultaneously opened up in someone else’s head – a perfectly timed witness was there to observe me collapse in the middle of the street. What are the chances that on the dark, deserted, and rain-soaked streets of sleepy Grosse Pointe, Michigan there would be a witness?! They’re spooky slim…

Apparently, it was not the time for my story to end. The witness – now far more a hero and life-long brother than witness – cradled me in the street, rain still pouring, until I could speak of the direction home – and then he carried me there…

The bloody scrapes, bruises and fat lip were caused by the initial face-plant and a series of subsequent falls along the half-block stumble home. I remember none of it. What came next was emergency open heart surgery – and a long, psychologically mind-twisting road back to put my entire life back together without anyone noticing…

Now, why do I think this detour is important to share? How could it possibly be related to Jump Trading? And, what does any of this have to do with Dave Grohl?! This is the point in the story that you begin to recall our well-worn quote from da Vinci about learning how to see that everything connects to everything else…

For starters, it turns out that ALL of the buyside-focused modeling and content that Alphacution has produced has come after my heart surgery; from the “Context Machine: Estimating Asset Manager Technology Spending” wherein we seek to validate (what would eventually turn out to be) our unified market hypothesis and establish the initial version of our asset management ecosystem map, to our recent (unprecedented) case studies on Citadel and Susquehanna International Group (SIG) – and, of course, the 127 posts that spilled out in between.

Moreover, it turns out that in the aftermath of this health event – and, I imagine this to be true of many others’ near-death episodes – I have experienced the bizarre phenomenon of a heightened sense of awareness, insight and flexibility of perspective. This is the primary dividend – the gift – of the ordeal. The ideas somehow arising – effortlessly – to my mind; the subtle details making themselves large and noisy in the right moments perhaps explained by the fact that I simply can no longer afford to allow life’s common penchant for pettiness and bullshit to weigh on my mind.

Now, you can play cynical from where you sit right now – and think it weirdly self-serving to digress this way – but it’s a fact, and I’m as mystified by it as anyone… My life is hanging by a thread; at least, now I know it…

So, in the spirit of what I perceive to be folks like Howard Stern’s or Joe Rogan’s primary contribution to the world – their honesty, openness and rawness, even if sometimes crude, sophomoric or excessively irreverent – I have made a deal with myself to leave everything on the field; to tell some of the behind-the-scenes personal stories along with the technical stories (while there is still opportunity to do so)…

In the immediate post-heart surgery darkness that was my mindset, one mantra – a song – seems to have helped encapsulate these sentiments and lubricate this second-chance road quite well, from Foo Fighters’ “Congregation”: “I’ve been going through life making foolish plans. Now my world is in your hands. Send in the Congregation.” This is the essence of what I needed to do…

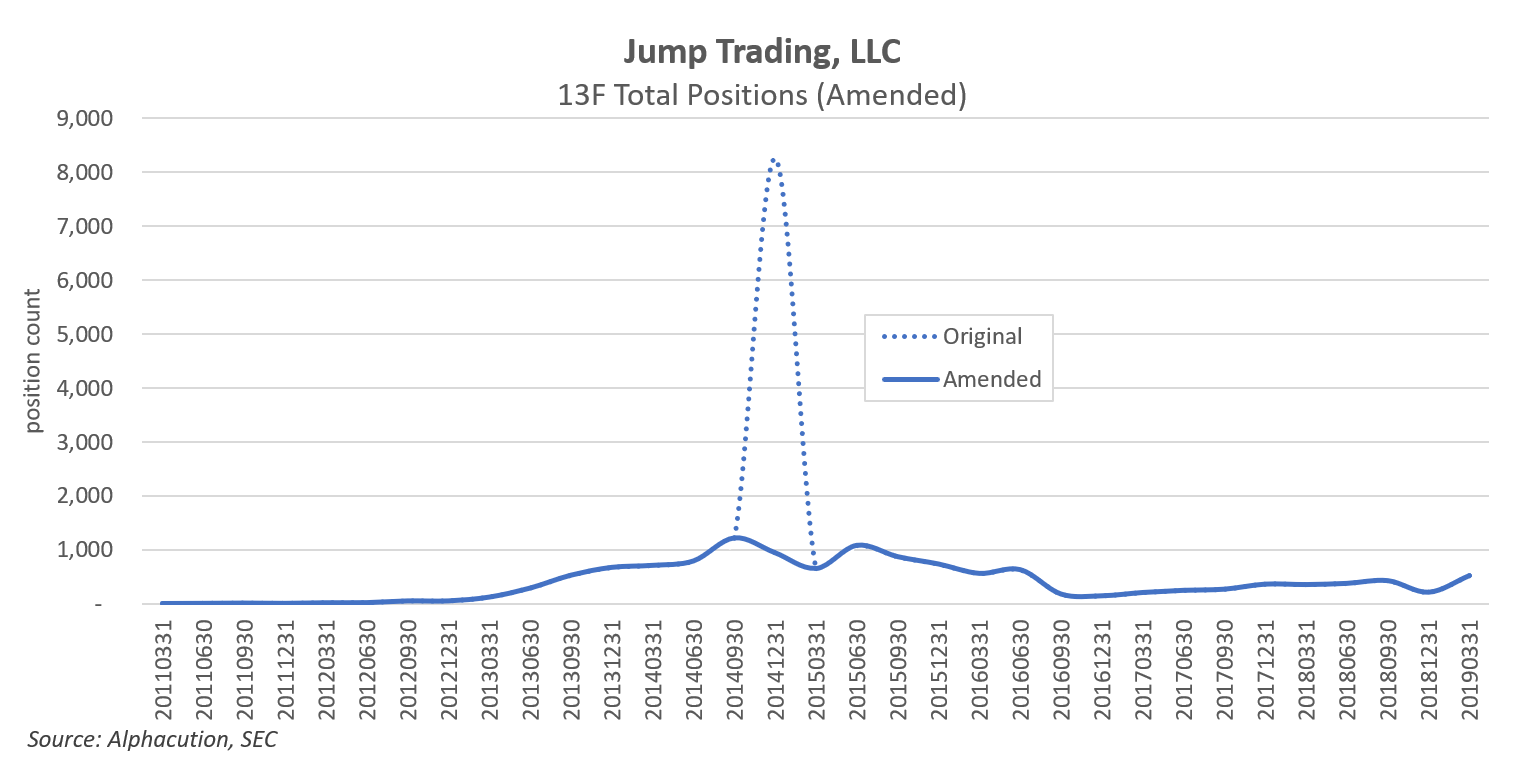

And so, it seems now, almost two years later, that there is a congregation here – a feedback loop made up of you and many others – that has taken shape by responding to the impacts of this work. One clue in support of this milestone brings us back to Jump Trading. On May 14, 2019 – precisely 31.11 seconds after filing its normal 13F report for Q1 2019 – Jump also files an amended 13F report (13F/A) for Q4 2014 wherein it corrects its total position count from the original 8,245 positions to 953 positions by reducing its options positions from 8,003 to 713 (see below).

It’s a very small clue, but clearly someone is paying attention at Jump. I mean, what are the chances that a firm like this files a 13F/A more than four years after the fact without an external catalyst? In the hundreds – maybe thousands at this point – of 13F reports that Alphacution has consumed since late 2017, I have never seen a lag of that duration. Most 13F/A’s are filed within days or weeks or – once in a blue moon – within a year, unless conditions of confidentiality have been established.

Now, there is much much more “congregational development” to be done here for sure, however, the feedback loop on the growing spectrum of impacts that this work appears to be having on the community of players is what truly makes this effort both fascinating and fun. And, because there are several other firms – marquee firms like Goldman Sachs and our case study subjects like Citadel and SIG – who also have missing regulatory reports or erroneous data in some of their filings, the expectation is that others will respond as Jump did – in addition, of course, to the now thousands of those (like you) that have begun to pay closer and closer attention to what is going on here.

From the bottom of my heart, thanks for that attention and the feedback…