“In playing ball, and in life, a person occasionally gets the opportunity to do something great. When that time comes, only two things matter: being prepared to seize the moment and having the courage to take your best swing.”

Hank Aaron

** The executive summary for Alphacution case study, “The Rise of Hudson River Trading,” is also available for free download (with registration) in our Reports Library **

Introduction

As if on cue, and apropos of the times, a tweet by Joe Gawronski, President of Rosenblatt Securities states that December 24, 2020 marked the first time ever that off-exchange trading represented the majority of US equity volume (50.38%):

Rewinding from there to a Reuters article dated January 16, 2018 entitled “Hudson River Trading to buy rival HFT firm Sun Trading,” HRT’s co-founder and director, Jason Carroll, said in a statement, “This acquisition combines HRT’s expertise in on-exchange trading with Sun’s expertise in off-exchange trading creating a stronger, more diverse firm.”

What happens between these two points in time is no accident. More than describing a theme that contributes to the disruption of the entire trading and asset management ecosystem, they are two milestones in the story that launches Hudson River Trading, LLC (HRT) into what Alphacution estimates is a rarefied league of proprietary trading firms that exceeded $1 billion in net trading revenue for 2020.

Until now, Alphacution has been intensely focused on shedding light on the broadest, most consequential trading firms in the global markets ecosystem. This led to our first-ever case studies on some of the most attention-grabbing names in the business. Legendary firms like Citadel Securities, Susquehanna International Group (SIG), Two Sigma and Jane Street are among our published works; a research library that is without peer.

These works were developed in parallel with a steady cadence of much shorter research excerpts published on our Feed, thereby exposing a much more diverse roster of notable players in total; each of which – short or long, deep or cursory – serving like pieces in the evolving solution to a much larger and more complex puzzle. As if writing a script for a Netflix series whose ending remains perpetually uncertain, each act of puzzle-solving – published, yet-to-be-published, or merely serving as backdrop – has incrementally illuminated a much clearer picture of this ecosystem. We have come to call this market macro-structure research.

It turns out that the legendary players to which we have dedicated our initial focus and deeper analysis have been valuable for more than their ability to fascinate. They are the cornerstones of the latest market structure phenomena, and therefore, have an extraordinary influence on the topology of the landscape, not only for the spaces they occupy but for the spaces they leave behind.

This is all perhaps an overly poetic way of introducing the nuts and bolts of the matter: There is a war being waged between what happens in the light and what happens in the dark.

More than describing any number of religious texts or sci-fi movie plots, the inherent inefficiencies caused by liquidity fragmentation, structured product mechanics, and derivative product mechanics have galvanized strategy selection for those who wield industrialized technology; creating unprecedented fissures in the trading and asset management ecosystem. Given the level of interconnectedness, this war at the epicenter of listed markets – most notably in the US – impacts all the major stakeholder groups. And, given the winner-take-all dynamics caused by pervasive technology adoption, the roster of firms who fall on the fortunate side of the competitive line is far shorter than the list that falls on the unfortunate side.

With few exceptions, bulge-bracket broker-dealers have struggled to compete with the world’s leading proprietary trading firms (all of which are registered broker dealers and often market makers, and whose ongoing financial success perpetuates a positive feedback loop that allows them to stay at the forefront of technical innovation and human capital attraction). Many hedge fund managers have struggled to adapt – much less, realize – that material component of the so-called alpha they once enjoyed as outsized performance is now being captured by those who stand much closer to the sources of liquidity.

Traditional asset managers, particularly those without a vibrant exchange-traded fund (ETF) franchise, also suffer from a lack of automation, speed, creativity, and adaptability. Solution vendors are plagued by a declining spicket of new prospects in a world that favors an incumbency of incumbents. And, last but certainly not least, the retail segment, particularly the subset of day traders, risk junkies and other thrill seekers, is largely entertained in the new, frictionless, and increasingly gamified environment. In short, the configuration at the center of listed markets – which, thanks to an historically-accommodative yield curve, is one of the only games in town – continues to cause tectonic shifts and existential risks throughout the entire global markets landscape.

At the base of all this, current market structure promotes a finite list of mainly speed-related arbitrage strategies, all of which reside within Alphacution’s structural alpha zone; the home of all hyperactive trading strategies[1]. With the Robinhood-triggered move – en masse – in November 2019 by the entire retail brokerage industry to a zero-commission framework (and fueled, in part, by new, more transparent SEC Rule 606 disclosures), 2020 is the year when the value of captive order flow elevated the war between dark trading and lit trading to an unprecedented level of obviousness that is now observable by the untrained eye.

Based on additional regulatory data beginning in late 2014, accumulated evidence shows that captive order flow is among the most recent in a set of keys used to unlock trading profits by those who dare to stand exceedingly close to capitalism’s furnace. More than matching order flow from a nested architecture of cooperatively affiliated strategies, captive order flow has proven to provide a peek at the future. No matter that much of the value of that signal decays quickly, sometimes in mere microseconds. Harnessing more captive order flow improves the predictive powers of that signal.

Except for Jane Street (who seems yet to fully embrace the wholesaling game), our case study subjects so far are leaders among a short list of wholesale market makers who are highly active in the realm of captive order flow, especially, captive retail order flow. This includes the combined practices of payments for order flow (PFOF), dark pools (including single dealer platforms – SDPs), and the most sophisticated high-performance technical infrastructure to leverage inherent inefficiencies caused, in large part, by liquidity fragmentation and derivative product mechanics (including both options and ETFs).

When you consider that 1) the available universe of securities is largely derivative of a subset of that inventory (whereby as much as two-thirds of tradeable securities in that universe are options and ETFs), 2) that the thirst for yield in the longstanding – if not, further deteriorating – interest rate environment supports persistent flows into equities, and 3) the increasing pervasiveness of quantitative methods, among other factors, have all conspired to foster increasing concentration of liquidity within that securities universe.

Literally a game of temporal fragments, it’s no wonder that the signal derived from captive order flows has become such an important variable in this equation. Moreover, the flywheel effect continues to speed up and cause further intensifying liquidity concentrations. Like the properties of fractals (where similar patterns recur at different scales), we see the patterns of increasing concentrations happening everywhere…

Even in the rarified air of the leading prop firms, there are notable fault lines. Citadel Securities and SIG are the only two of these to have found success – if not, dominance – across the broadest spectrum of hyperactive strategies that include all listed product classes, many asset classes, and most regions. Alphacution believes that the primary source of this dominance is a market making platform that successfully spans both cash equity and equity option markets, among others. Jane Street Group is currently the only other player with the maturity, knowledgebase, and scale to be in position to mount a credible competitive threat against these top two (or in front of many other contenders), and therefore, Alphacution ranks it as the #3 global player in the structural alpha game.

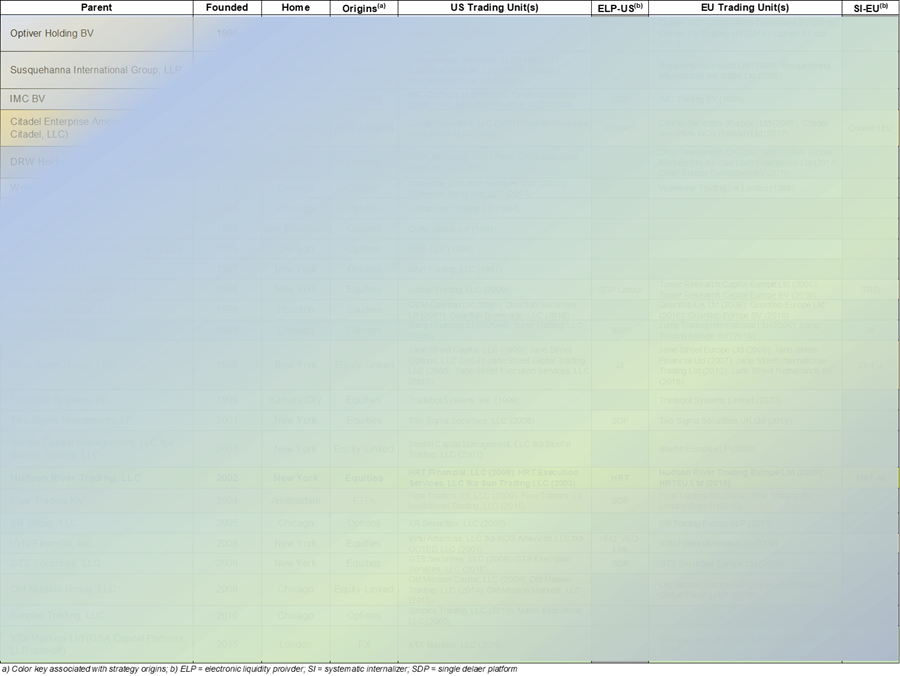

Of course, given windfalls earned by many prop trading firms in 2020 off the back of historic volumes and volatility, competitive dynamics in the areas of market making and other hyperactive strategies could shift starting as early as this year. If that happens, the players are likely to come from the following roster of leading proprietary trading firms and their trading affiliates (see Exhibit 1A, below).

Exhibit 1A: 25 Leading Proprietary trading Firms w/ US and EU Trading Affiliates, by Founding Year

Nevertheless, we need to draw a line between those few with the broadest strategy spectrum and greatest scale and then everyone else, at least for the time being. After this line comes the next tier of players who tend to have a more focused spectrum of strategies which are more highly tethered to a single product class, such as cash, options, or futures. This is where the subject of this case study on Hudson River Trading, LLC comes into the picture. Furthermore, given the market dynamics and competitive impediments outlined above, it is becoming increasingly more challenging to scale a trading business. HRT is unique amongst its competitors for navigating the terrain to a dramatically new level of scale over the past three years. Overcoming these challenges was made possible by the acquisition of Sun Trading, LLC in Q1 2018. That event is a centerpiece for the story that follows…

Data Sample

The Storyboard and select findings contained in this report represent Alphacution’s interpretation of a total of at least 73 regulatory reports representing Hudson River Trading, LLC (HRT), its predecessors and certain affiliated entities, including (most notably) HRT Financial, LP (HRTF), HRT Execution Services, LLC (HRTX, formerly known as Sun Trading, LLC), Hudson River Trading Europe Limited (HRTE), and Sun Trading International Limited (STI), among others. The supporting data sample is comprised specifically of the following:

- 24 quarterly 13F[2] holdings reports (including 13F-HR/A amendment reports, wherever applicable) for the 6-year time range beginning December 31, 2014 (or, Q4 2014) and ending September 30, 2020 (or, Q3 2020) for HRT Financial, LP (HRTF; formerly known as HRT Financial, LLC as of November 2020);

- 9 annual FOCUS reports (on Forms X-17A-5 and X-17A-5/A, wherever applicable) for the years ending December 31, 2011 thru December 31, 2019 filed by HRT Financial, LP (HRTF; formerly known as HRT Financial, LLC as of November 2020) with the SEC, FINRA and SIPC;

- 16 annual FOCUS reports (on Forms X-17A-5 and X-17A-5/A, wherever applicable) for the years ending December 31, 2004 thru December 31, 2019 filed by HRT Execution Services, LLC (HRTX; formerly known as Sun Trading, LLC for the period beginning 2004 and ending 2017) with the SEC, FINRA and SIPC;

- 11 full account reports disclosing financial and operational data for the years ending December 31, 2009 thru December 31, 2019 filed by Hudson River Trading Europe Ltd (HRTE) with the United Kingdom’s registrar of companies, Companies House;

- 13 full account reports disclosing financial and operational data for the years ending December 31, 2005 thru December 31, 2017 filed by Sun Trading International Limited (STI; formerly known as EOS Trading Limited for the years 2005, 2006 and 2007) with the United Kingdom’s registrar of companies, Companies House;

- Any other peripheral data or content referenced in this report that was available from open and public sources or searchable on the surface internet; and,

- Contextual modeling, exhibits, case studies, Feed posts and/or any other pre-existing content from Alphacution’s research library.

Note: Both Hudson River Trading Europe Ltd (HRTE) and HRTEU Limited (Dublin) submit best execution venue reports for RTS 27 and 28 under MiFID II due to their status as systematic internalisers (SIs). As of the development of this report, any modeling that may result from this data remains in process, and therefore, not included in this case study.

Furthermore, in US equivalence to European SIs, HRT Execution Services (HRTX) is known as an electronic liquidity provider (ELP). ELPs, alternative trading systems (ATSs), national exchanges, and other market centers typically file monthly Rule 605 reports on order execution quality for “covered orders” in National Market System (NMS) stocks. Orders for which customers request special handling are excluded from the definition of covered orders. Though Alphacution identified Rule 605 reports on covered orders for many other ELPs – like Citadel Securities, GTS Securities, IMC Financial Markets, Jane Street, Two Sigma Securities, Virtu Financial, and Latour Trading – HRTX’s 605 reporting consistently reported “no covered orders.”

No representative of Alphacution has been in contact with any representative of Hudson River Trading, LP or affiliated entities for the preparation of this report. This report is solely based on the author’s interpretation of Alphacution’s ongoing assembly of raw, publicly available data; library of contextualized modeling; and internally developed content. This report does not benefit from, nor include any material non-public information (MNPI).

[1] For details on Alphacution’s ecosystem map, structural alpha zone, and/or hyperactive trading strategies (among other discoveries), see “Appendix III – Landscape.”

[2] Form 13F is a quarterly report filed, per United States Securities and Exchange Commission regulations, by “institutional investment managers” to the SEC and containing all position-level equity assets under management of at least $100 million in value with relevant long US holdings. All US-listed equity securities (including ETFs, equity options, and convertible bonds) in the manager’s portfolio are included and detailed according to the issuer name, security description, the security identifier (i.e. – CUSIP number), position value, number of shares, and other attributions. As of June 30, 2020, Alphacution estimates that the full list of Form 13F securities count totals 17,425 securities. Short positions are not required to be disclosed and are not reported. Form 13F covers institutional investment managers, which include registered investment advisers (RIAs), banks, insurance companies, hedge funds, trust companies, pension funds, mutual funds, among other natural persons or entities with investment discretion over its own account or another’s. Form 13F is required to be filed within 45 days of the end of a calendar quarter. Find more about the 13F dataset on the Alphacution Feed.